basilh@virginia.edu

@basilhalperin

Originally posted as a Twitter thread.

How much of Chinese growth is *TFP growth* vs ‘merely’ Solow catch-up growth?

A mini lit review, for the purpose of attracting real experts to correct my errors 🤠

The natural background to the China question is the lit on the rapid growth of Japan + the East Asian Tigers (Hong Kong, Singapore, South Korea, Taiwan), on which I recently gave an opinionated summary

Something like half of East Asian Tiger growth was from TFP growth – call it 3% per year

As context, US TFP growth over this period was ˜1%. So 3% is pretty fast!

=> Tiger growth seems to have been not just Solow-style catch-up growth (again, see previous thread)

Okay, well what about China?

How much of Chinese growth has been from actually producing things more intelligently, ie TFP growth, versus just “adding more machines to the economy, shuttling more kids through school”?

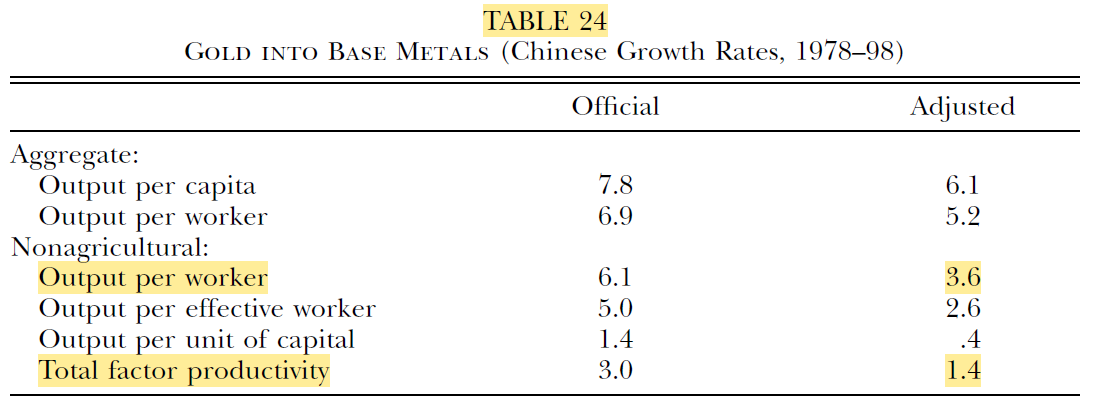

Again starting with Alwyn Young, the 2003 paper (“Gold Into Base Metals”, his amazing trademark deadpan):

He estimates 1.4% TFP growth 1978-1998 – not that high, but still accounting for ˜75% of [non-ag] growth (!)

(the “Adjusted” column uses an alternative GDP deflator)

Aside: in this paper Young switches from the traditional growth accounting method (used in eg Young 1995) to the adjusted (“Harrodian”) method I described – which properly attributes the growth caused by capital accumulation induced by higher TFP, to TFP

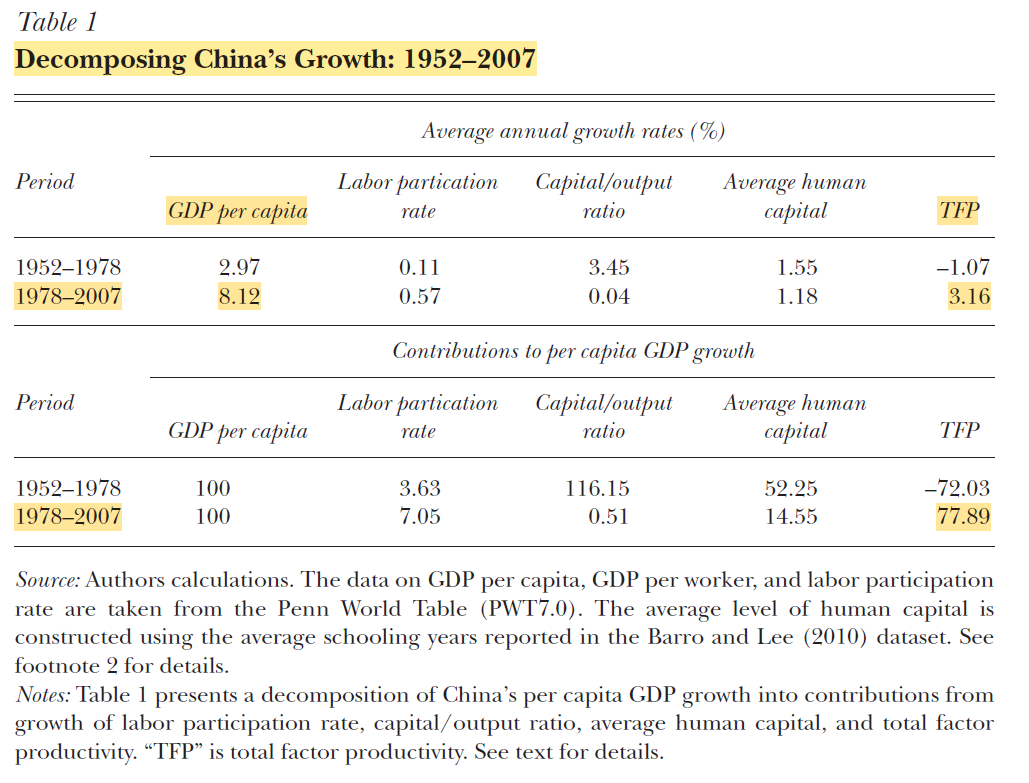

Brandt and Zhu (2010) revise Young’s estimate even further up – with updated data and correcting the deflator. Zhu (2012, JEP) is a very readable summary, showing:

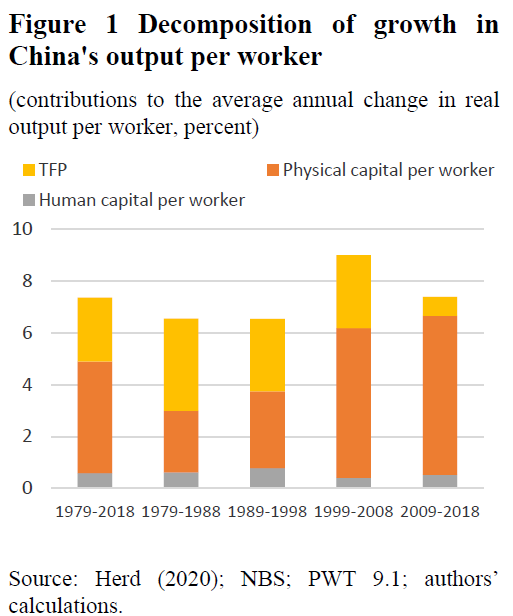

From 1978-2007, TFP growth averaged 3.2% per year (!!) – again accounting for more 3/4 of GDPpc growth

You can also see in that^ table an accounting for growth under Mao, 1952-1978: 3% growth in GDP per capita [on avg 💀], entirely due to K+H accumulation – annual TFP growth was -1%!!

If I had to recommend one paper here, it would be this Zhu (2010) paper

Will also note – Cheremukhin, Golosov, Guriev, and Tsyvinski (2015, 2024) do an interesting wedge accounting of the Chinese economy, mostly discussing pre-reform but also briefly post-reform. I’m not sure if their results match the rest of this thread

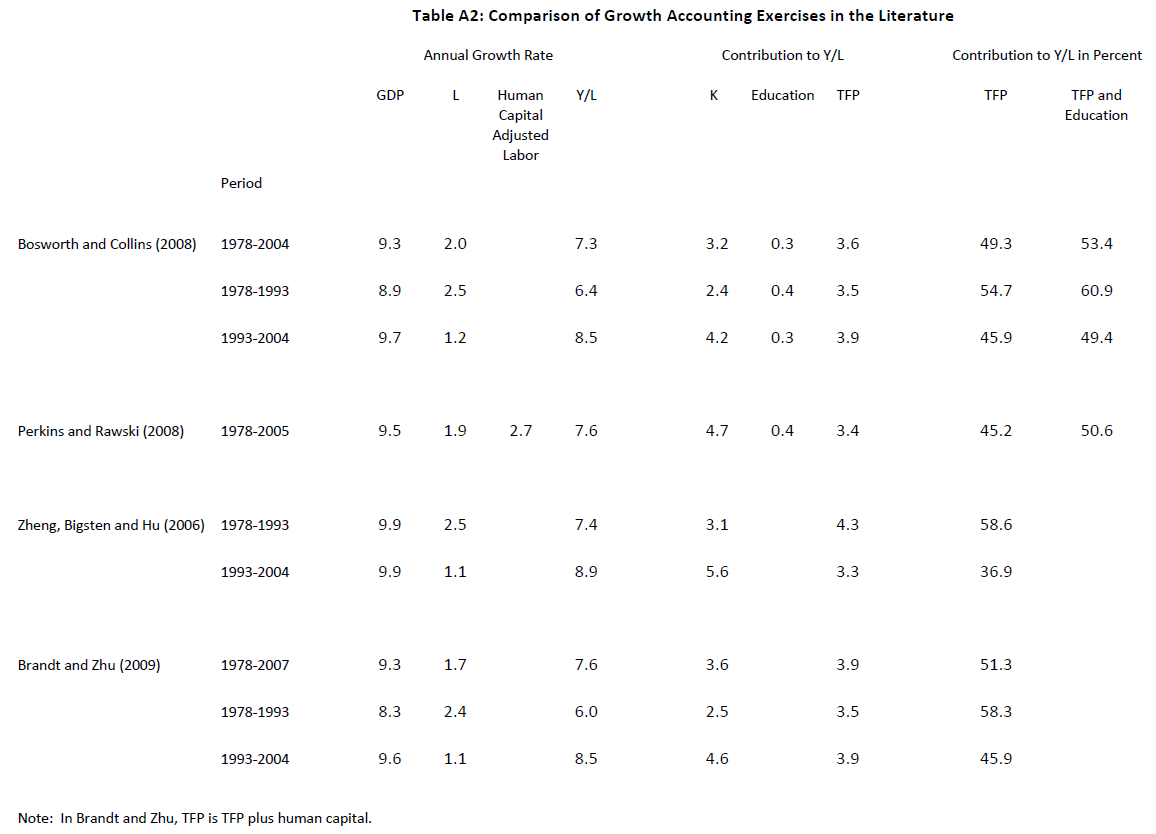

Other growth accounting papers covering the period up to 2008 also show 50-75% of Chinese growth is accounted for by TFP growth (Bosworth and Collins 2008; Zheng, Bigsten, and Hu 2009; Rajah and Leng (2022))

Ok, well that was part 1: TFP growth in China was high 1978-2007, accounting for 75% of Chinese growth over the period (after being quite negative under Mao)

Part 2 is: TFP growth has slowed down, a lot, since 2008 and the Great Recession

I haven’t been able to find any fantastic papers doing a growth accounting for the last decade (please send!!) and have been unwilling to wade into the data myself beyond the offensively crude cut I did here

BUT all the available evidence points to a major slowdown in Chinese TFP growth since 2008:

Brandt et al (2020) estimates a pre-2008 ten-year annual TFP growth of 2.8%

vs.

Post-2008 ten-year annual TFP growth of 0.7%

Rajah and Leng (2022) do a classic growth accounting decomposition, and also find TFP growth slowing substantially in the 2010s

Plausibly this slowdown is due in part to distortions caused by the policies enacted to avoid the global Great Recession?

Again, I would love to read more analysis of the Chinese TFP slowdown of the last 15 years / the Xi Jinping economy, please send links 😀

Ok, so:

1. Part 1 was that Chinese TFP growth was high after the reform & opening up

2. Part 2 was that TFP growth slowed substantially post-2008

What’s the future of Chinese growth?

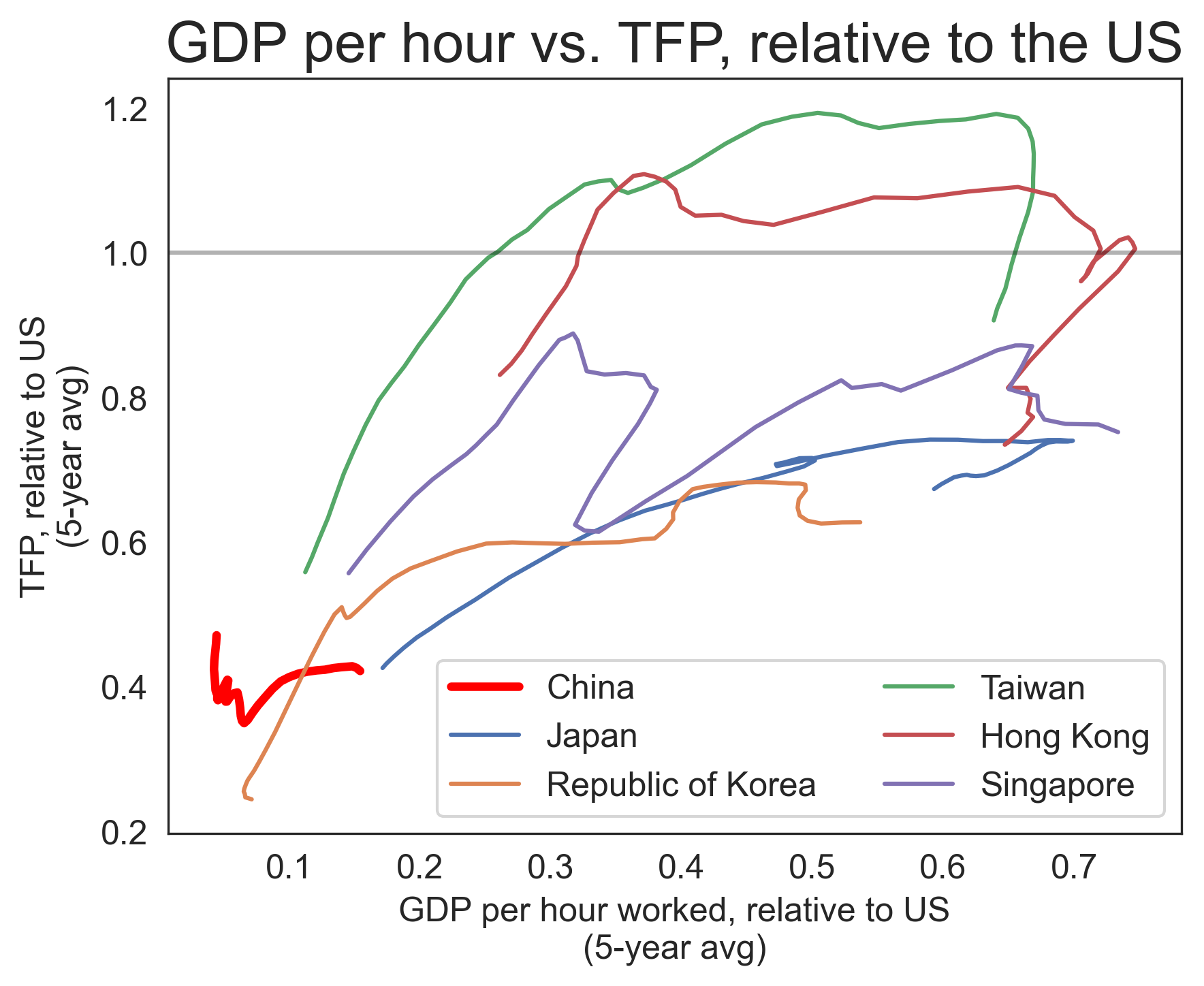

The fundamental fact is that Chinese TFP is still far below that of the US: there is a lot of room left to run. China could still grow a lot. Obviously, the question is: will it?

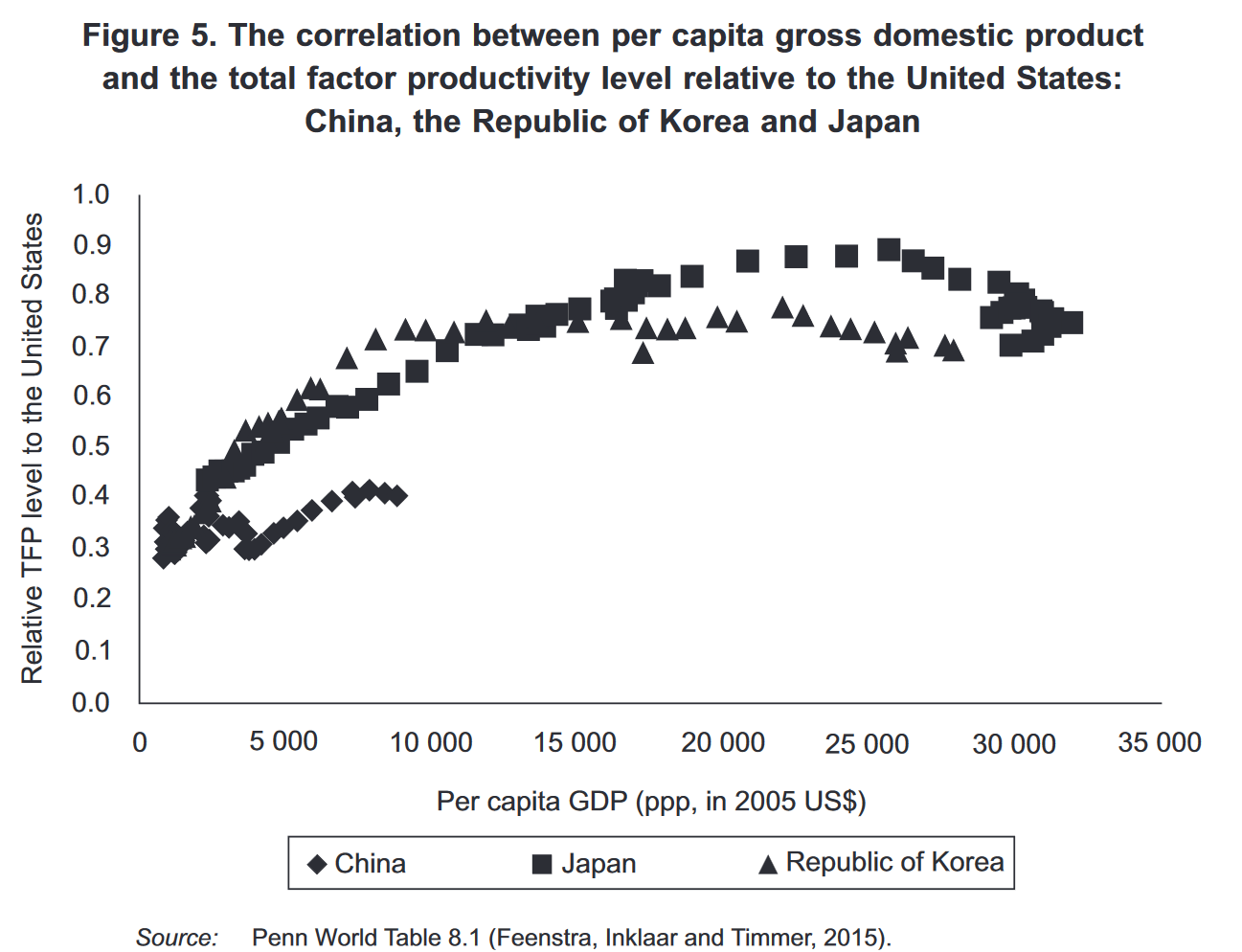

Zhu (2012) points out: in the ˜30 years post reform and opening up, China went from 3% of US TFP to 13% (in 2007)

In comparison:

Japan TFP 1950: 56% of US -> 83%

Korea TFP 1965: 43% of US -> 63%

Taiwan TFP 1950: 50% of US -> 80%

Again: China has a lot of room left to run...

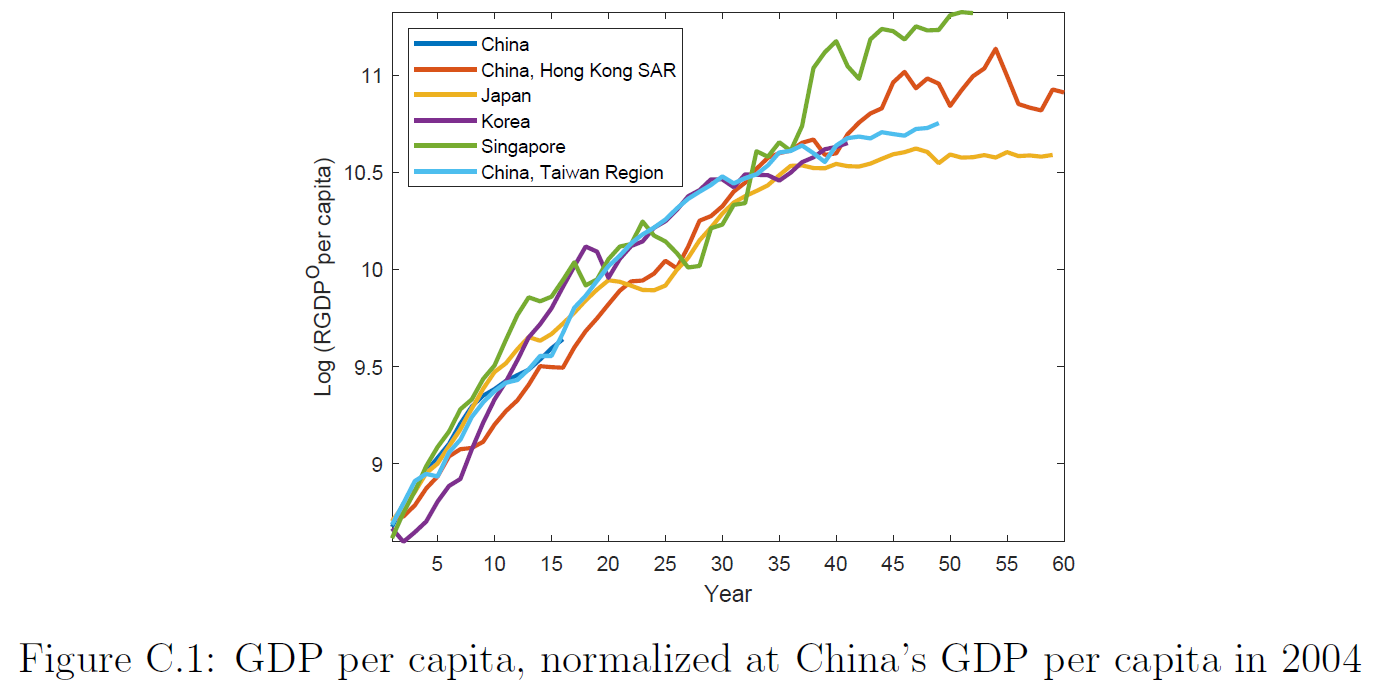

Here’s my quick and liable-to-be-incorrect figure showing “Chinese productivity has a lot of room left to grow”:

Plotting the Y/L trajectory for major East Asian economies vs. TFP – data simply pulled from PWT. Chinese TFP is low

(That same PWT data, though, also shows Chinese TFP being flat relative to the US over the last 60 years, which contradicts the main thesis of this thread, so…

¯\_(ツ)_/¯)

(I would assume the PWT TFP estimate quality <<< the quality of the cited papers)

Anyway –

The best analysis that I could find on projecting future Chinese growth [modulo the singularity etc] is Rajah and Leng (2022), which uses a neoclassical framework

Rajah and Leng (2022) assume a continued gradual reduction in Chinese TFP growth until convergence to frontier TFP growth rates

Between a TFP slowdown, an aging population, and declining {urban population, housing, public investment} growth –

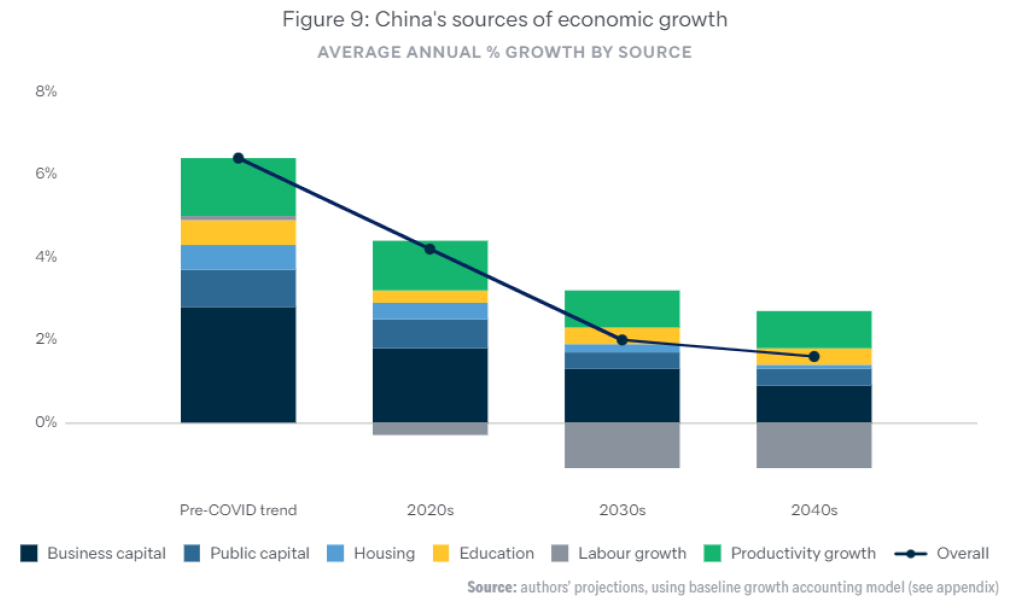

They forecast 3% GDP growth by 2030

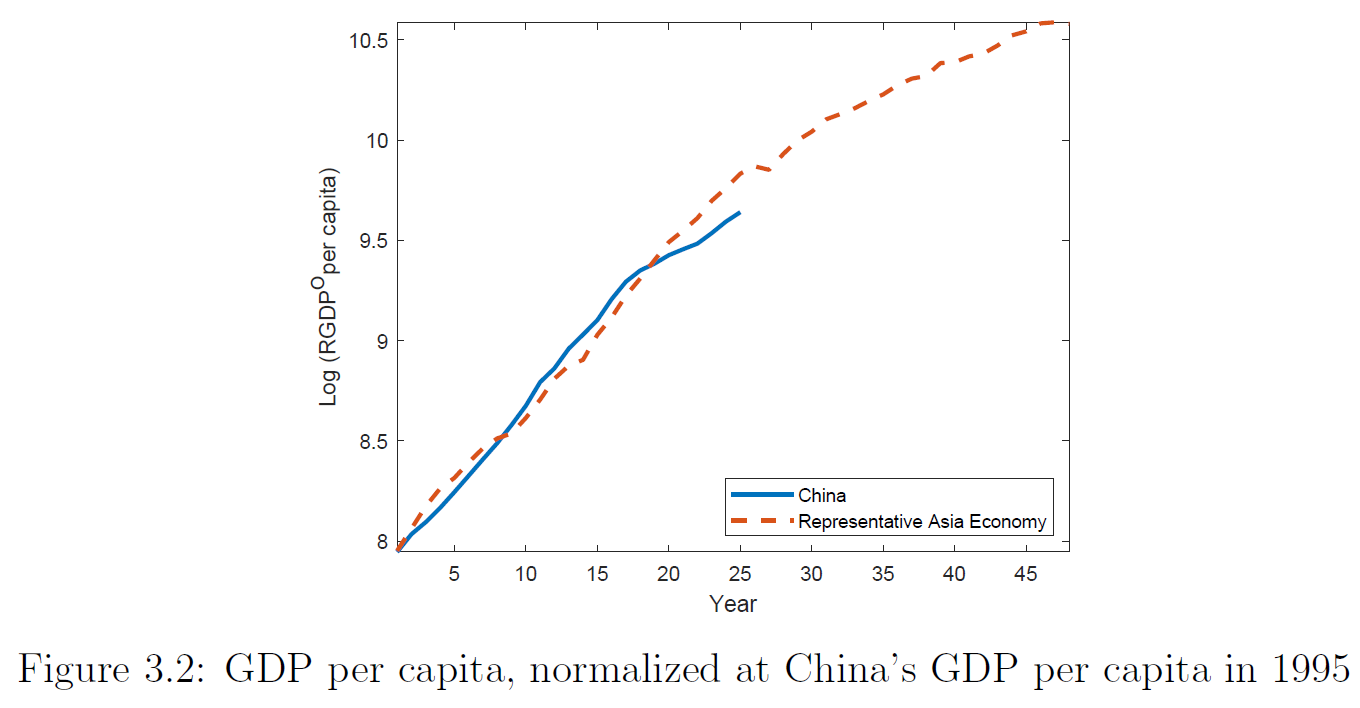

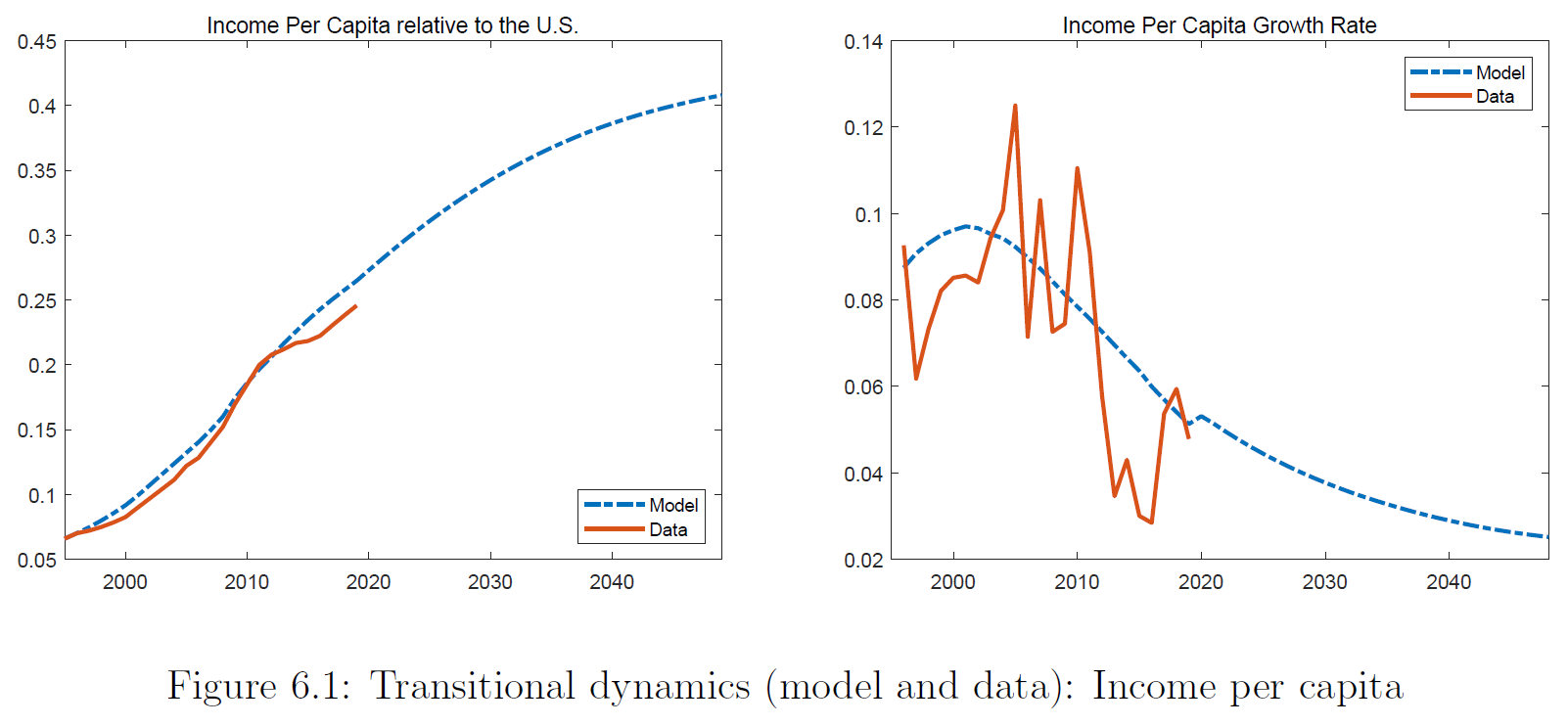

An even more direct approach to projecting future Chinese growth is Fernandez-Villaverde, Ohanian, and Yao (2023), where TFP growth is projected statistically

The idea is: China’s growth path has followed shockingly closely to other East Asian miracles. What if that continues:

Again, additional references/corrections welcome

These threads brought to you by some binge reading before a big trip to China last month. Cold War II sucks but at least we’ve still got growth accounting 👍So that’s my read of the China growth accounting lit:

1. TFP growth was fast + was an important part of the miraculous decades of growth, which rejects crude Solow-ism

2. TFP growth has slowed down since 2008

3. There is a lot of room left that the PRC could run

Some bonus China economy charts from my lit binge:

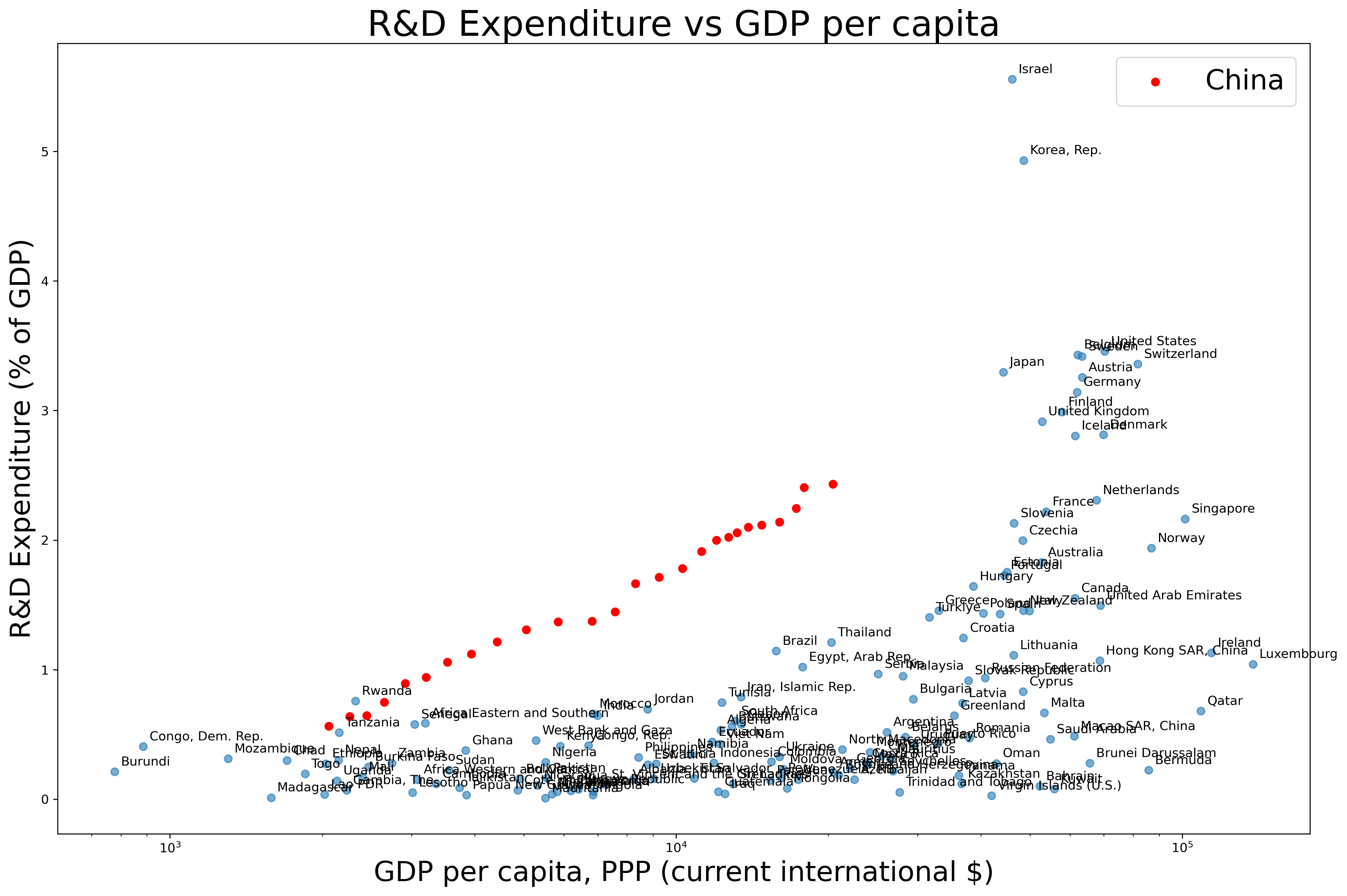

1) China is spending more on R&D than you would expect based on GDP per capita

(my update of a chart from Wei, Xie, and Zhang 2017)

2) Consensus long-term China real GDP growth forecasts:

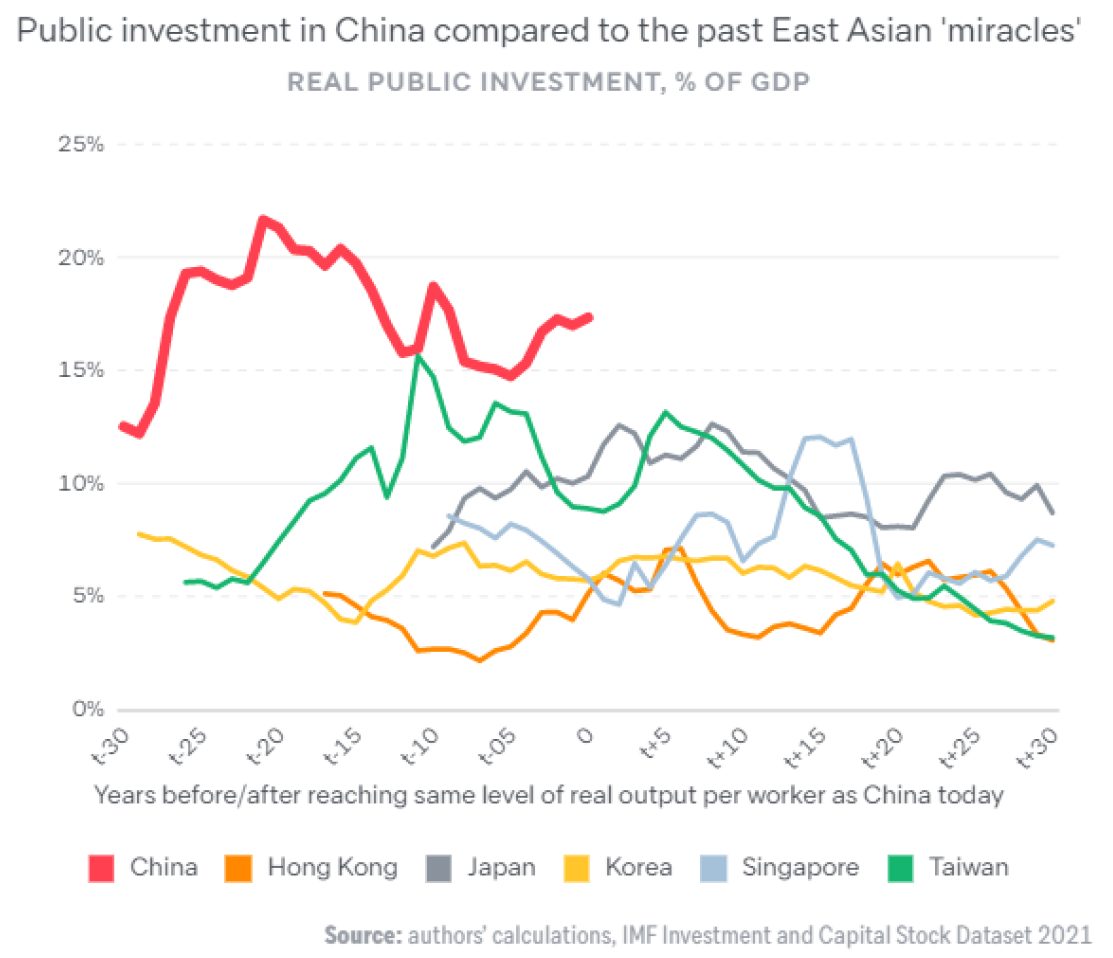

3) Chinese public investment has been higher than other East Asian miracles over the whole development trajectory (Rajah and Leng 2022):

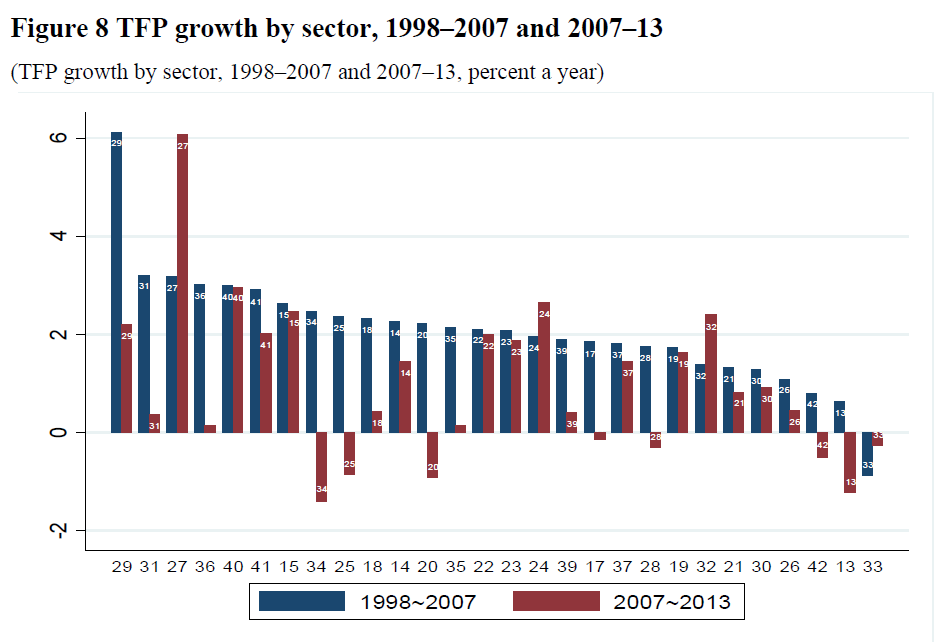

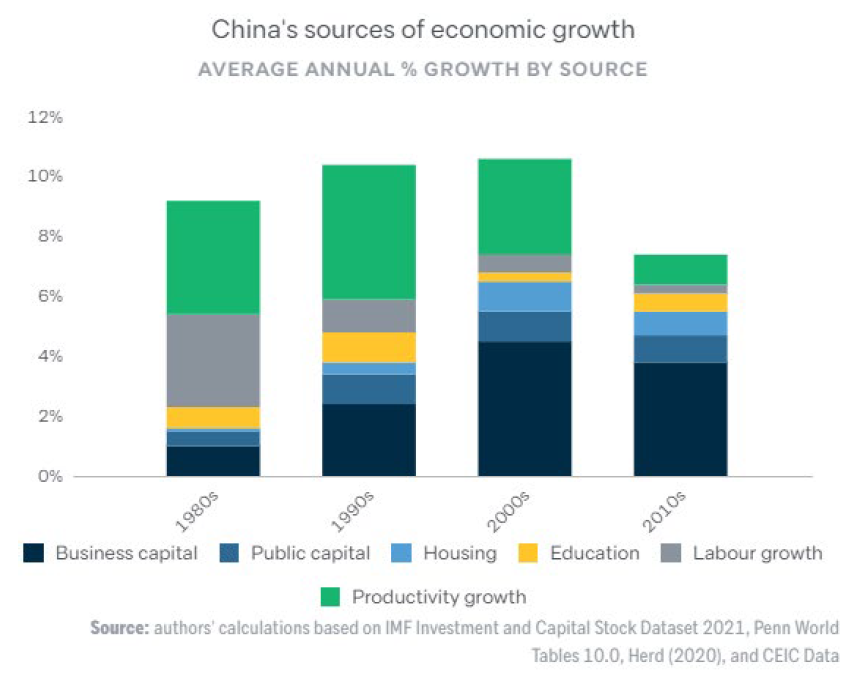

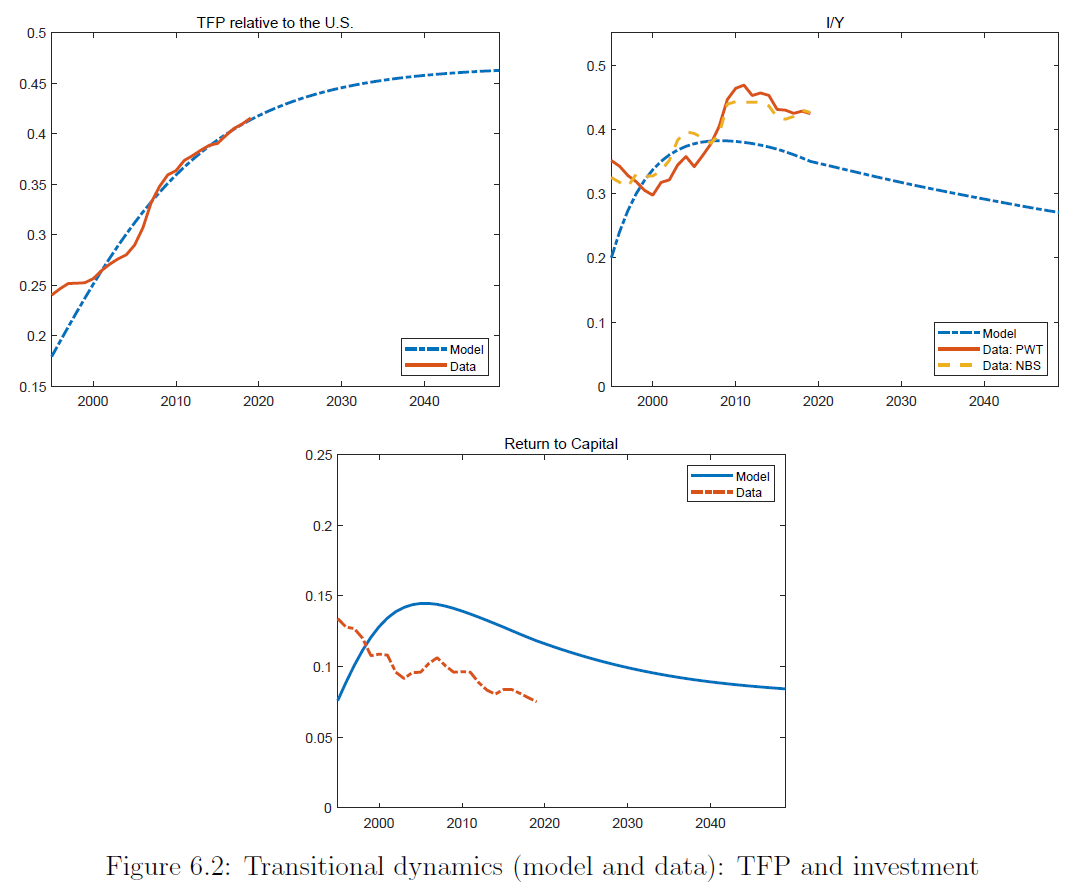

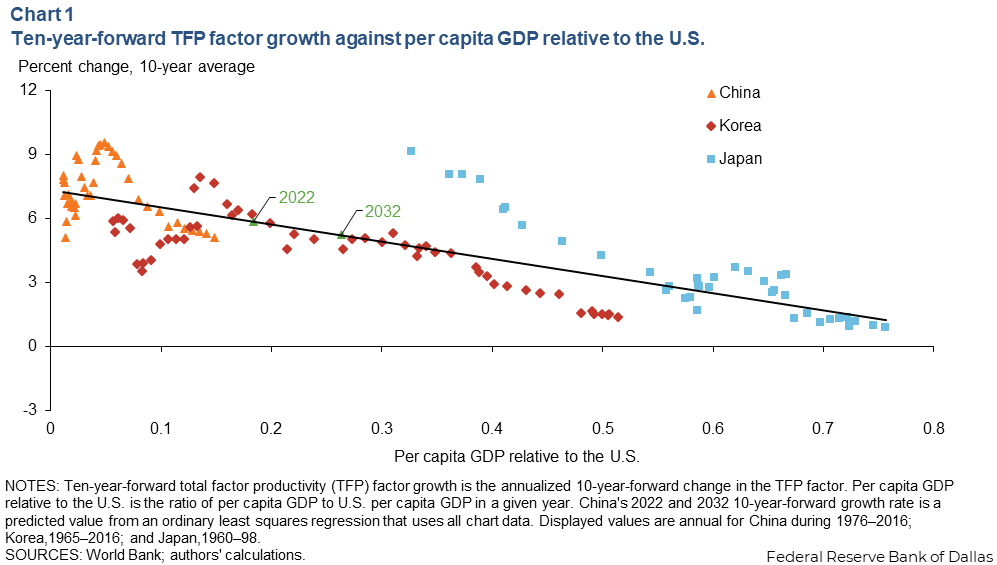

4) I haven’t looked closely into these TFP charts but they are interesting and plausibly more accurate than my similar quick and dirty one: (source 1, source 2

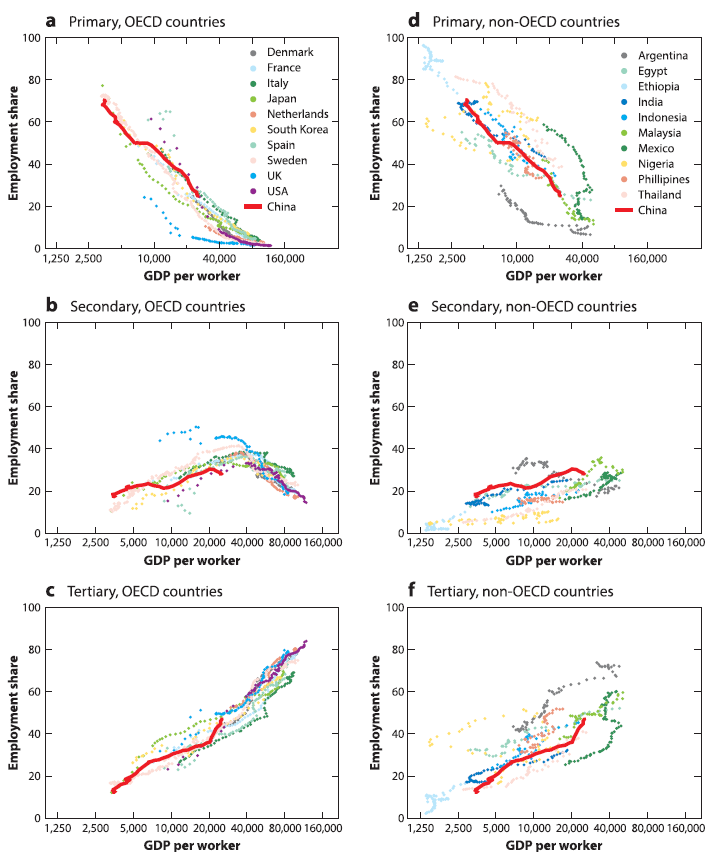

5) The Chinese economy is shifting towards services; and this trajectory is surprisingly predictable across countries (Chen, Pei, Song, and Zilibotti 2023)

[primary = agriculture; secondary = manufacturing; tertiary = services]

Bonus book recommendation: Yasheng Huang

Will hopefully do a thread on this but Yasheng Huang’s EAST is probably the best big think book on China I’ve read + great “applied political economy theory”

— Basil Halperin (@BasilHalperin) June 2, 2024

Bonus podcast recommendation: Yasheng Huang interview