basilh@virginia.edu

@basilhalperin

Original post:

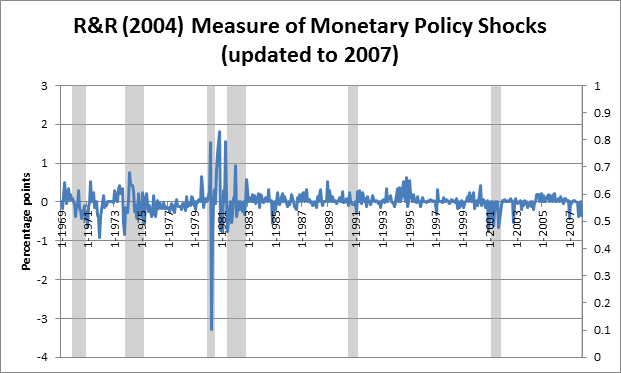

I've updated the Romer and Romer (2004) series of monetary policy shocks. The main takeaway is this graph of monetary policy shocks by month, since 1969, where the gray bars indicate recession:

When the two published their paper, they only had access to date up through 1996, since Fed Greenbooks – upon which the series is based – are released with a large lag. I've updated it through 2007, the latest available, and will update it again next month when the 2008 Greenbooks are released.

The two interesting points in the new data are

Below I'll go into the more technical notes of how this measure is constructed and my methodology, but the graph and the two points above are the main takeaway.

How is the R&R measure constructed?

First, the Romers derive a series of intended changes in the federal funds rate. (This is easy starting in the 1990s, since the FOMC began announcing when it wanted to change the FFR; before that, the two had to trawl through meeting minutes to figure it out.) They then use the Fed's internal Greenbook forecasts of inflation and real growth to control the intended FFR series for monetary policy actions taken in response to information about future economic developments, specifically RGDP growth, inflation, and unemployment.

In other words, they regress the change in the intended FFR around forecast dates on RGDP growth, inflation and unemployment. Then, as they put it, "Residuals from this regression show changes in the intended funds rate not taken in response to information about future economic developments. The resulting series for monetary shocks should be relatively free of both endogenous and anticipatory actions."

The equation they estimate is:

The Romers show in their paper that, by this measure, negative monetary policy shocks have large and significant effects on output and the price level.

It is worth noting the limitations of this measure. It is based on the federal funds rate instrument, which is not a very good indicator of the stance of monetary policy. Additionally, if the FOMC changes its target FFR between meetings, any shock associated with that decision would not be captured by this measure.

Results

First, I replicated the Romer and Romer (2004) results to confirm I had the correct method. Then I collected the new data in Excel and ran the regression specified above in MATLAB. The data is available here and here (though there might have been errors when uploading to Google Drive).

The residuals are shown above in graph form; it is an updated version of figure 1a in Romer and Romer (2004).

The coefficients and statistics on the regression are (this is an updated version of table 1 in the original paper):

Last, for clarity, I have the monetary policy shock measure below with the top five extremes removed. This makes some periods more clear, especially the 2007 shock. Again, I will update this next month when the 2008 Greenbooks are released. It should be very interesting to see how large a negative shock there was in 2008.